Architectural Exposition and Macro-Systemic Vulnerability Analysis of the Financial Sustainability System (SSF) - Part II

Navigating the Dichotomy Between Theoretical Compliance and Empirical Execution in the Brazilian Football Economy.

RECAPITULATION OF MODULES I & II

Part I of this essay established the Systemic Deleveraging Protocol and executed a Forensic Diagnosis of the four foundational pillars governing the Financial Sustainability System (SSF). The analysis isolated a fundamental shift from organic fiscal synchronization toward a Capital Adequacy Paradigm, where institutional solvency is tethered to the Ultimate Beneficial Owner’s (UBO) liquidity rather than internal operational velocity.

The preceding modules identified three critical Model Incongruencies that threaten the framework’s integrity:

Synthetic Denominator Dilation: The tactical use of formalized equity injections to artificially expand the expenditure perimeter of the Squad Cost Indicator (SCI), neutralizing the Macro-Systemic Wage Deflation Vector.

Maturity Profile Arbitrage: The reclassification of current liabilities to depress Net Short-Term Obligations (OLCP) ratios through end-of-year accounting engineering and high-cost bridge financing.

Distressed Asset Liquidation Loops: The erosion of long-term competitive equity (youth talent) to satisfy rigid, short-term Zero-Arrears Mandates and prevent immediate registration bans.

PART II: SYSTEMIC COUNTER-MEASURES AND LONG-TERM EQUITY VALUATION IMPACTS

INTRODUCTION: INTERIM SYNTHESIS AND ARCHITECTURAL RECAPITULATION

Part I of this essay executed a Forensic Diagnosis of the Financial Sustainability System (SSF), isolating the Squad Cost Indicator (SCI) and Net Short-Term Obligations (OLCP) as the primary governors of institutional liquidity. The analysis established that the SSF functions not as a purely organic fiscal synchronizer, but as a Capital Adequacy Mandate that permits Synthetic Compliance through the Equity-Absorption Mechanism. Key forensic risks identified included Denominator Dilation, Maturity Profile Arbitrage, and the Externalization of Remunerationvia off-balance-sheet vehicles. Part II now pivots to the macro-systemic evaluation of the ANRESF governance architecture and the deconstruction of latent Regulatory Arbitrage Vectors.

MODULE III: MACRO-SYSTEMIC CRITICAL EVALUATION OF THE SSF FRAMEWORK

THE GOVERNANCE ARCHITECTURE AND REGULATORY ENFORCEMENT PARADIGM

The Private-Public Regulatory Hybridity Gap

The macro-architecture of the SSF attempts to establish a pseudo-governmental regulatory agency, the National Authority for Financial Responsibility in Sport (ANRESF), within a private associative framework. This creates a Regulatory Hybridity Gap, where an entity seeks to enforce complex financial restructuring and anti-trust mandates—specifically targeting Multi-Club Ownership (MCO)—without the benefit of sovereign statutory authority. This reliance on Contractual Compliance rather than legislative mandate necessitates a system of Administrative Soft Law that remains highly vulnerable to the scrutiny of the broader civil legal environment and Statutory Preemption challenges.

ANRESF Autonomy and Anti-Trust Protocols

The SSF incorporates advanced corporate governance mechanisms designed to insulate the regulatory process from Political Capture and Cross-Ownership Fiduciary Friction:

Institutional Independence and Quarantines: The establishment of ANRESF as a functionally independent body requires a Twenty-Four Month Cooling-Off Period for directors transitioning from club-affiliated roles. This is a critical barrier against Regulatory Capture, ensuring that the regulatory overlay remains untethered from individual institutional agendas.

MCO Thresholds and Significant Influence: The framework utilizes a strict Ten Percent Voting Rights Threshold as the technical trigger for Significant Influence. Crossing this threshold in more than one competing entity necessitates Forced Asset Divestitures or the placement of equity into Neutralization Blind Trusts. This is designed to mitigate Collusive Competitive Behavior and the monopolization of talent pipelines.

Insolvency Event Expenditure Neutralization: Upon the filing of a Judicial Reorganization (RJ), the framework mandates an immediate cap on personnel expenses, restricted to a Six-Month Historical Average. This prevents the Moral Hazard of using court-protected cash flow to artificially inflate the competitive value of the squad while senior creditors remain impaired.

SCENARIO E: THE ANTI-TRUST BLIND TRUST CHALLENGE

An international private equity group acquires an 80% stake in Club Alpha (a Tier-1 SAF). Simultaneously, the same group holds a 15% stake in Club Beta through a subsidiary. Under the SSF, this triggers a Conflict of Interest Event. The group is forced to either divest the 15% stake or transfer the voting rights of Club Beta to a certified independent Neutralization Vehicle. If the group attempts to maintain operational control via shared data platforms or scouting networks, ANRESF must identify this De Facto Operational Control without the benefit of sovereign subpoena power, testing the limits of Associative Enforcement Velocity.

Neutralizing Competitive Moral Hazard in Distressed Environments

The insolvency containment protocols redefine the lifecycle of a distressed football entity. Historically, the Brazilian market permitted Predatory Insolvency, where clubs utilized bankruptcy stays as a Competitive Subsidy—freezing debt payments to fund aggressive squad expansion.

Sanitized Restructuring: The SSF forces reorganization to be an exercise in Operational Contraction. By limiting spend to historical averages, it ensures that the entity’s competitive capacity is proportional to its actual Solvency Status.

Market Stabilization: This acts as a barrier against Systemic Risk Contagion, ensuring that distressed entities do not distort the market price of labor using unpaid capital.

SCENARIO F: THE REORGANIZATION RESTRAINT Club Gamma enters acute fiscal distress and files for Judicial Reorganization to halt a BRL 200 million debt collection. Historically, the club would use the BRL 5 million monthly “debt service savings” to sign elite strikers. Under the SSF, the club’s payroll is locked at its six-month historical average. This prevents the club from utilizing the bankruptcy stay as a competitive subsidy. The club is forced to focus on Creditor Satisfaction Protocols and streamlining operations rather than aggressive market expansion.

Forensic Evasion and Beneficial Ownership Obfuscation

The primary vulnerability within Module III lies in the Burden of Proof required to execute forced divestitures or identify illegal cross-ownership.

Complex Capital Stacks: Institutional investors utilizing tiered holding structures, offshore Special Purpose Vehicles (SPVs), or algorithmic debt-covenants can exert Significant Influence while technically remaining below the 10% equity detection threshold.

Forensic Enforcement Deficit: ANRESF lacks the legislative authority to Pierce the Corporate Veil. The agency must rely on voluntary disclosure or inter-federation information sharing, which is often subject to significant Information Asymmetry.

Enforceability Timeline: Within the fast-moving registration windows, the delay required to prove Ultimate Beneficial Ownership (UBO) in foreign jurisdictions can render anti-trust measures practically unenforceable, allowing Stealth MCOs to operate until a terminal legal discovery occurs.

SCENARIO G: THE SHELL-COMPANY STRATAGEM

A global sports holding company seeks to control two Brazilian Tier-1 clubs without triggering divestiture rules. It acquires 90% of Club A directly. For Club B, it utilizes three different offshore SPVs, each acquiring 9% of voting shares (27% total). On paper, no single entity exceeds the 10% threshold. The SSF requires ANRESF to prove Commonality of Interest. Without the power to audit international bank transfers in tax havens, ANRESF may be unable to verify the violation, leaving the integrity of the league in a state of High-Density Risk.

MODULE IV: LATENT VULNERABILITIES AND STRUCTURAL DEFICITS

FORENSIC DECONSTRUCTION OF SYSTEMIC ARBITRAGE VECTORS AND GOVERNANCE FRICTION

Introduction: The Forensic Stress Test

Module IV executes a high-density forensic deconstruction of the latent vulnerabilities embedded within the Financial Sustainability System (SSF). While Modules I through III define the theoretical boundaries of compliance, Module IV isolates the Forensic Friction Points where regulatory intent is neutralized by institutional-grade arbitrage. This analysis identifies the “Arbitrage Voids” that allow sophisticated market participants—specifically Sovereign Wealth Funds and Institutional Private Equity—to maintain Super-Systemic Competitive Advantage while appearing compliant. It serves as a stress test of the framework’s ability to survive Reflexive Control maneuvers, Statutory Preemption challenges, and Actuarial Recognition Inconsistencies in an emerging market environment characterized by high informational opacity.

Divergence from International Accounting Standards (IFRS)

Executive Thesis: The SSF utilizes a fragmented and permissive local accounting framework (PCAB/ITG 2003) rather than mandating rigid, unadulterated International Financial Reporting Standards (IFRS). This creates a fertile environment for Life Cycle Recognition Inconsistency and Balance Sheet Obfuscation, allowing entities to report artificial health while harboring toxic underlying liabilities.

Empirical Rationale: The allowance of local GAAP tailored for non-profit entities enables, for example, the Capitalization of Intangible Assets and the deferral of liabilities under methodologies that diverge sharply from global norms regarding Revenue from Contracts with Customers and Financial Instruments.

Systemic Impact Vectors: This misalignment structurally misprices the Brazilian football market. Institutional investors conducting cross-border due diligence face a data environment where reported earnings and net equity are untethered from global valuation baselines, demanding the application of steep Opacity Discount Premiums.

SCENARIO H: THE SIGNING-ON FEE DEFERRAL ARBITRAGE

A club pays an Unattached Athletic Asset (Free Agent) a BRL 50 million signing-on fee. Under IFRS, this is treated as an immediate expense or amortized strictly over the contract length. Under local ITG 2003, the club capitalizes this as an “Intangible Marketing Right,” spreading the impact to avoid a spike in the Squad Cost Indicator (SCI). The club appears compliant with the 70% ceiling while its actual Expenditure Velocity is hemorrhaging capital.

Heterogeneity in Financial Statement Presentation

Executive Thesis: The absence of a rigidly codified, algorithmic Standardized Chart of Accounts (SCoA)—beyond the broad mandates of ITG 2003 (R2) —introduces severe informational asymmetry. This lack of granular taxonomy neutralizes the capacity for automated, high-fidelity peer benchmarking and allows for the exploitation of Revenue Recognition and Competence (Accrual) Principle “gray zones.”

Empirical Rationale - Revenue Recognition Divergence: While the SSF and PROFUT demand audited statements, they permit heterogeneous treatment of multi-period cash inflows. Clubs frequently engage in “Revenue Frontloading,” recognizing the entirety of a multi-year transfer receivable or broadcast tranche in the current fiscal year to artificially inflate the SCR (Squad Cost Ratio) denominator, despite the underlying Competence Principlemandating periodic distribution.

Competence Principle Erosion: There is a systemic failure to align the “matching principle” between high-value player acquisitions and their corresponding revenue streams. Clubs exploit the gap between Cash Flow (actual installments) and Accrual (accounting recognition), often deferring the recognition of “Performance-Related Bonuses” to future cycles while recognizing 100% of sponsorship income upfront.

Classification Arbitrage: In another example no unified rule strictly dictates whether Intermediary/Agent Commissions are classified as Operational Expenditures (OPEX) or capitalized into the Intangible Asset Basis. This allows clubs to fluctuate their reported cost ratios for identical economic behaviors, effectively hiding wage-bill pressure within the balance sheet.

Systemic Impact Vectors: The presentation variance exponentially increases the friction and cost of institutional capital deployment. It forces the ANRESF to abandon automated oversight and conduct manual, forensic reconciliation of every balance sheet to extract a normalized view of the league’s economic reality, undermining the Duty of Information established in Article 64 of the Lei Geral do Esporte (LGE).

ADVERSARIAL SCENARIOS (THE GAPS)

SCENARIO I(a): THE “ADMINISTRATIVE EXPENSE” DUMPING GROUND

The Play: Club A is at 69.5% of its 70% SCR limit. To sign a new technical director, they classify the massive image rights component of the contract as “Institutional Marketing and Corporate Branding” under general administrative costs rather than “Sporting Personnel Remuneration.”

The Result: Without a line-by-line standardized taxonomy under ITG 2003 (R2), the ANRESF’s automated flags fail to trigger, allowing the club to maintain a Hidden Over-Leveraged Labor Force while technically appearing compliant.

SCENARIO I(b): THE “COMPETENCE BYPASS” REVENUE SURGE

The Play: Facing a massive deficit that would trigger APFUT exclusion, a club “anticipates” a 2027 broadcast tranche by selling the receivable to a financial vehicle at a discount. Instead of recognizing only the 2026 portion (the Competence Principle), the club records the full net amount as “Other Operating Income” in the current period.

The Result: This bypasses the spirit of Article 25 of the PROFUT Law (Prohibition of Revenue Anticipation). The club “cleans” its current SCR and deficit metrics, effectively starving future administrations of the revenue required to sustain the squad in the next cycle, creating a “Financial Cliff” event.

Auditor Oversight and Principal-Agent Vulnerability

Executive Thesis: The SSF exhibits a critical vulnerability by failing to establish a centralized oversight board for independent auditors, leaving the system exposed to Complicit Actuarial Manipulations.

Empirical Rationale: The regulatory framework accepts the auditor’s signature as absolute proof of compliance. However, empirical precedent demonstrates the practice of permitting the Immediate, Non-Discounted Capitalizationof long-term future cash flows (e.g., 50-year broadcasting rights) as present-day equity.

Systemic Impact Vectors: This failure destroys the integrity of the Indebtedness and Sustainability pillars. By allowing future receivables spanning decades to be booked at nominal value today—ignoring the Time Value of Money—clubs manufacture Phantom Equity Surpluses, shielding insolvent entities from sanctions.

SCENARIO J: THE FIFTY-YEAR PHANTOM EQUITY BOOST

The Play: A club sells its media rights for the next 50 years for a nominal BRL 1 billion. Instead of recognizing this as Deferred Revenue (a liability to be recognized over 50 years) or calculating the Net Present Value (NPV)—which might be only BRL 200 million—the auditor allows the club to book the full BRL 1 billion as an Asset/Equity Boost.

The Result: This “Phantom Equity” allows the club to absorb massive operational deficits while technically showing positive Net Equity. It masks a state of Terminal Fiscal Decay, allowing the club to remain compliant with licensing while functionally insolvent.

Fragility of Self-Regulation vs. Statutory Jurisdiction

Executive Thesis: The SSF operates as an associative construct without Statutory Preemption under Federal Law, rendering its enforcement highly vulnerable to Protracted Civil Injunctions.

Empirical Rationale: Under the Brazilian Constitution, the law cannot exclude any injury from judicial appreciation. Punitive actions (relegation, transfer bans) will inevitably be challenged in state-level civil courts rather than specialized sporting tribunals.

Systemic Impact Vectors: The lack of hard legal backing creates a terminal threat to Operational Velocity. If a club successfully obtains a Preliminary Injunction (Tutela de Urgência) to suspend a ban, the deterrence value of the entire framework drops to zero.

SCENARIO K: THE BIFURCATED LEAGUE REALITY

A Tier-1 club is relegated by ANRESF for solvency violations. The club sues in its home state, and a local judge grants a preliminary injunction forcing the CBF to keep them in the first division. The league schedule collapses, and international broadcasters trigger Force Majeure clauses to exit contracts, leading to Systemic Revenue Evaporation.

Remuneration Package Arbitrage (Image Rights Bifurcation)

Executive Thesis: The SSF’s ability to capture true Squad Cost is compromised by the historical bifurcation of wages into labor contracts and “Image Rights” agreements, creating a vector for Off-Balance-Sheet Remuneration.

Empirical Rationale: Clubs often utilize third-party commercial vehicles or offshore entities to pay “performance bonuses” that are never recorded in the labor-related payroll monitored by the SSF, utilizing Bifurcated Labor Arbitrage.

SCENARIO L: THE OFFSHORE BONUS VECTOR

A club registers a salary of BRL 1 million with the CBF. Simultaneously, an offshore entity owned by the club’s Ultimate Beneficial Owner (UBO) signs a “Global Image Licensing” deal with the player for BRL 2 million. The SSF only “sees” the BRL 1 million, meaning the club’s reported squad cost is only 33% of its actual commitment, rendering the 70% cap Mathematically Cosmetic.

Associative Residual Governance and Asset Lock-In

Executive Thesis: The transition to a Sociedade Anônima do Futebol (SAF) often leaves the original association with “Class A” (Golden Share) rights. This creates an Operational Paralysis Risk where the association weaponizes its residual governance—not for identity preservation, but as a lever for Judicial Predation. The SSF’s metrics fail to quantify the “Litigation Friction Cost,” which allows a minority stakeholder to neutralize foreign capital through low-merit, high-disruption legal injunctions.

Empirical Rationale: Under Article 2, § 3º of Law 14.193/2021 (SAF Law), the association retains specific veto powers (name, shield, colors, and relocation). However, “Legal Malware” is introduced when associations initiate Baseless Rescission Actions or Injunctions (Liminares) seeking to annul the SAF constitution or debt-transfer tranches. These maneuvers, often lacking substantive legal basis, exploit the slow pace of the Brazilian judicial system to force “settlements” or “buy-backs” from foreign investors, effectively treating the SAF as a Hostage Asset.

Systemic Impact Vectors: The threat of “Predatory Litigation” creates a Capital Freeze. Foreign investors, sensing Judicial Insecurity, halt mandatory capital tranches (Aportes), triggering the SSF’s Solvency Alarms and inadvertently pushing the club toward the Sanction Grid due to artificial liquidity traps.

SCENARIO M(a): THE ASSET LIQUIDITY DEADLOCK

The Play: A SAF fails its Indebtedness Indicator and attempts to sell a non-core training facility for BRL 60 million to satisfy the ANRESF Solvency Mandate. The Association uses its Golden Share/Class A status to block the sale under the guise of “Historical Preservation” or “Indivisibility of Patrimony.”

The Result: The SAF is forced into a Registration Ban (Transfer Ban) despite possessing sufficient Book Value Assets to clear its debt. This illustrates a failure of Asset-Liability Synchronization, where “Symbolic Vetoes” outweigh “Fiscal Solvency.”

SCENARIO M(b): THE LITIGATION PARASITE (JUDICIAL OVERREACH)

The Play: A minority association, dissatisfied with the SAF’s technical performance, files a “Public Civil Action” (Ação Civil Pública) or a Contractual Annulment in a local provincial court, alleging “Vices of Consent” in the original SAF valuation from years prior.

The Result: Although the lawsuit lacks a technical basis under the SAF Law, the local court grants a Preliminary Injunction freezing the SAF’s bank accounts until the merits are heard. The foreign investor ceases all investment, the Squad Cost Ratio (SCR) skyrockets as revenue halts, and the club suffers a Regulatory Collapse—not because of market failure, but due to Judicial Asymmetry.

Fiscal Moral Hazard and Amnesty Recurrence

Executive Thesis: The political economy of recurring tax amnesties (e.g., PROFUT) creates a Fiscal Moral Hazard that undermines the Solvency Mandate by incentivizing the intentional accumulation of tax debt.

Empirical Rationale: Clubs “settle” massive tax debts by entering new government refinancing programs with minimal down payments, satisfying the SSF’s Documentary Requirement while leaving Long-Term Leverage dangerously high.

SCENARIO N: THE REFINANCING REBOUND

A club is BRL 40 million behind in taxes. A new federal amnesty law is passed. The club joins the program, paying only BRL 2 million upfront to receive a “Clean Tax Certificate.” ANRESF clears the club, though it has effectively increased its total debt principle while masking it as a “bridge” to the next election cycle, maintaining a Perpetual Debt Cycle.

Inter-Jurisdictional Value Leakage (MCO Arbitrage)

Executive Thesis: The Cost Control pillar is vulnerable to Upstream Value Extraction, where player registration rights are undervalued in Brazil to maximize profits in secondary jurisdictions within a Multi-Club Ownership (MCO)network.

Empirical Rationale: MCO controllers can use a “sister club” to acquire players at prices that “optimize” the Squad Cost denominator through Synthetic Profit Generation.

SCENARIO O: THE ARTIFICIAL DENOMINATOR EXPANSION

A SAF sells an average youth player to its sister club in Portugal for BRL 50 million (market value: BRL 5 million). This BRL 45 million “profit” is added to the SSF denominator, allowing the Brazilian club to spend an additional BRL 31.5 million on salaries the following season. This is a Non-Organic Revenue Injection disguised as a transfer.

Market Value Distortion in Affiliated Sponsorships

Executive Thesis: Clubs within Multi-Club Ownership (MCO) networks utilize Non-Arms-Length Sponsorshipsto artificially inflate the denominator of the Squad Cost Indicator.

Vulnerability: The SSF lacks a robust Fair Market Value (FMV) Assessment Panel. Owners can execute Revenue Characterization Arbitrage—paying BRL 100M for a BRL 10M shirt sponsorship—effectively injecting equity disguised as commercial revenue to bypass SCR limits.

SCENARIO P: THE SPONSORSHIP INFLATION PUMP

The Play: An MCO-owned SAF signs a “Global Technology Partnership” with the owner’s holding company for BRL 150M. Independent auditors value the market exposure at BRL 15M.

The Result: The club “washes” BRL 135M of capital injection as operational revenue, lowering its reported SCR from 95% to 68%, avoiding an ANRESF transfer ban through Revenue Characterization Arbitrage.

Systemic Currency Exposure and Amortization Volatility

Executive Thesis: The mismatch between a BRL-denominated revenue environment and EUR/USD-denominated player assets creates Amortization Volatility that the SSF fails to buffer.

Vulnerability: Under FIFA Circular 1840 (5-year amortization cap), a sharp devaluation of the Brazilian Real increases the BRL-denominated amortization cost of foreign acquisitions overnight. This triggers Involuntary Regulatory Default, pushing a club over the 70% SCR limit due to macroeconomic fluctuations rather than operational mismanagement.

SCENARIO Q: THE CURRENCY-INDUCED SCR BREACH (Ref. IV.J)

The Play: A club signs three European players for €30M total. A 25% BRL devaluation occurs.

The Result: The BRL-denominated amortization load on the balance sheet spikes by BRL 7.5M annually. Despite no new wage increases, the club’s SCR crosses the 70% threshold, triggering an Involuntary Regulatory Default.

Beneficial Ownership and Stealth Operational Control

Executive Thesis: Sophisticated debt instruments, such as Convertible Notes, allow lenders to exert Significant Influence over a club’s sporting decisions without crossing the 10% equity threshold defined in the SAF Law.

Vulnerability: A single creditor could hold restrictive covenants over multiple competing clubs (e.g., veto rights on budgets or player sales). This creates a Fiduciary Arbitrage Void, where Shadow Governance is exercised through the capital stack rather than the equity table.

SCENARIO R: THE CONVERTIBLE DEBT PUPPETEER

The Play: A private equity firm holds Convertible Notes in three SAFs. The contract includes a “Negative Covenant” preventing any player sale below BRL 50M without the lender’s signature.

The Result: The lender dictates the transfer market strategy for 15% of the league while holding 0% voting shares, bypassing MCO restrictions and creating Collusive Competitive Behavior.

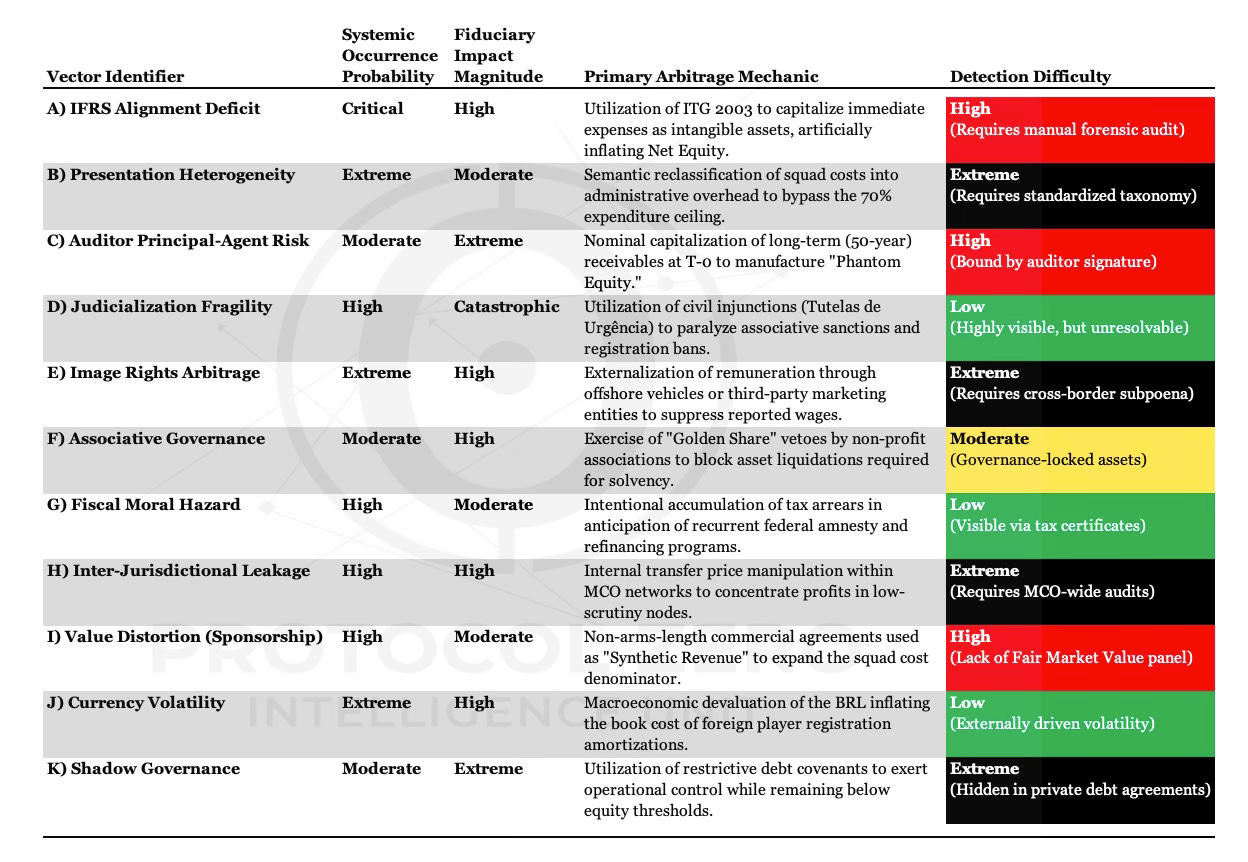

MODULE V: COMPOSITE RISK AND SYSTEMIC VULNERABILITY MATRIX

Forensic Mapping of Regulatory Arbitrage and Fiduciary Exposure

This matrix provides a high-density evaluation of the latent vulnerabilities identified within the Financial Sustainability System (SSF). It categorizes each deficit by its Systemic Occurrence Probability (SOP) and its Fiduciary Impact Magnitude (FIM), isolating the specific mechanics used for regulatory evasion.

CRITICAL PATH ANALYSIS OF THE MATRIX

1. The “Phantom Equity” Nexus (A, C, G) The intersection of IFRS Alignment Deficits, Auditor Negligence, and Fiscal Amnesty creates a recursive loop of fictitious capitalization. By booking 50-year TV deals at nominal value and deferring signing-on fees, clubs can present a “compliant” balance sheet while their actual liquid position remains terminal. This is a Primary Systemic Risk that threatens the credibility of the entire Brazilian SAF market.

2. The Jurisdictional Collision Course (D, F) The matrix highlights a fundamental conflict between the Lex Sportiva(internal football rules) and the Sovereign Legal Environment. The ability of state-level civil courts to grant injunctions against ANRESF sanctions represents a Terminal Vulnerability. Until the SSF is granted statutory preemption, the enforcement of points deductions and relegations remains purely theoretical and subject to indefinite legal paralysis.

3. The MCO Arbitrage Loop (H, I, K) Multi-Club Ownership models are currently positioned to extract Structural Alpha by exploiting the lack of Fair Market Value (FMV) assessments. By shifting value through sister-club transfers and inflated sponsorships, these entities can maintain a higher “Spend Velocity” than organic associative clubs, leading to an inevitable and deregulated market stratification.

OPERATIONAL SYNTHESIS & TERMINAL VERDICT

The Enforcement-Authenticity Gap (Fiduciary Failure)

The Composite Risk Index (CRI) of the Financial Sustainability System (SSF) yields a definitive conclusion: while the framework has achieved a high degree of fidelity in identifying the necessary Fiscal Parameters for measurement, it suffers from a terminal Structural Enforcement Deficit. The SSF currently lacks the Forensic Subpoena Power and Statutory Preemption required to pierce the corporate veil of sophisticated Sovereign Wealth and Private Equitycapital stacks. This creates a state of Regulatory Asymmetry, where compliance is verified via self-reported, certified documentation that remains vulnerable to Actuarial Recognition Inconsistency and Off-Balance-Sheet Externalization.

Strategic Risks for Institutional Liquidity Providers

For a Sovereign Wealth Fund or Institutional Investor, the primary risk is not the presence of regulation, but the Forensic Arbitrage Voids within that regulation. These voids facilitate the persistence of Non-Performance-Indexed Liabilities—previously termed “Toxic Unpaid Capital”—allowing competitors to maintain a higher Competitive Velocity through:

Synthetic Equity Buffering: Neutralizing operational deficits via non-organic capital infusions.

Maturity Profile Camouflage: Utilizing high-cost bridge financing to temporarily depress short-term leverage ratios for audit dates.

Jurisdictional Injunction Arbitrage: Leveraging the absence of federal statutory backing to paralyze enforcement via the civil court system.

Definitive Synthesis

The SSF, in its current iteration, transitions the Brazilian market from a state of “Unregulated Chaos” to a state of “Regulated Opacity.” The framework successfully establishes the benchmarks for Capital Adequacy and Operational Equilibrium, but until the ANRESF is fortified with legislative authority and IFRS-Mandated Standardization, the market will remain bifurcated. Institutional capital must apply a significant Opacity Discount Premium to all domestic assets, recognizing that “compliance” within the SSF is often a function of Accounting Engineering rather than genuine Economic Solvency.