Systemic Liquidity Capture

The SpaceX IPO, Index Benchmark Alterations, and Structural Mechanics of Public Wealth Risk Transfer

EXECUTIVE SUMMARY

This white paper details a highly anomalous structural shift occurring within global equity benchmarks ahead of the scheduled June 12, 2026 public listing of SpaceX under the ticker symbol $SPCX. Historically, public equity indexes (specifically the S&P 500, Nasdaq-100, and FTSE Russell) operated as strict quality-control layers designed to shield passive retirement portfolios from the volatility and unproven valuations typical of late-stage private market listings.

However, explicit rule amendments enacted in early 2026 have structurally transformed these benchmarks. By eliminating legacy profitability criteria and radically condensing standard “seasoning” periods down to windows as narrow as five trading days, the index architecture has been converted into a mechanism that mandates over $30 trillion in passive index-tracking retirement and 401(k) capital to buy SpaceX shares at their absolute valuation apex.

This document analyzes the technical micro-structures, hidden institutional conflicts, and regulatory loopholes that make this programmatic risk transfer legal. The findings indicate that rather than reflecting natural public market demand, the $SPCX listing operates as a highly engineered vehicle designed to absorb private venture capital concentration and subsidize massive, debt-fueled AI infrastructure burn rates at the expense of passive index fund total returns.

1. THE INTELLIGENCE VECTOR: FINANCIAL ANATOMY OF $SPCX

To dissect the structural premium engineered into the $SPCX IPO, the underlying corporate consolidation must be forensically unbundled. The core surface narrative emphasizes SpaceX’s historic hegemony over space launch mechanics and the robust subscription economics of the Starlink satellite network. However, the internal financial anatomy disclosed in the confidential, recently leaked S-1 prospectus tells a vastly different operational story.

The xAI Capital Absorption

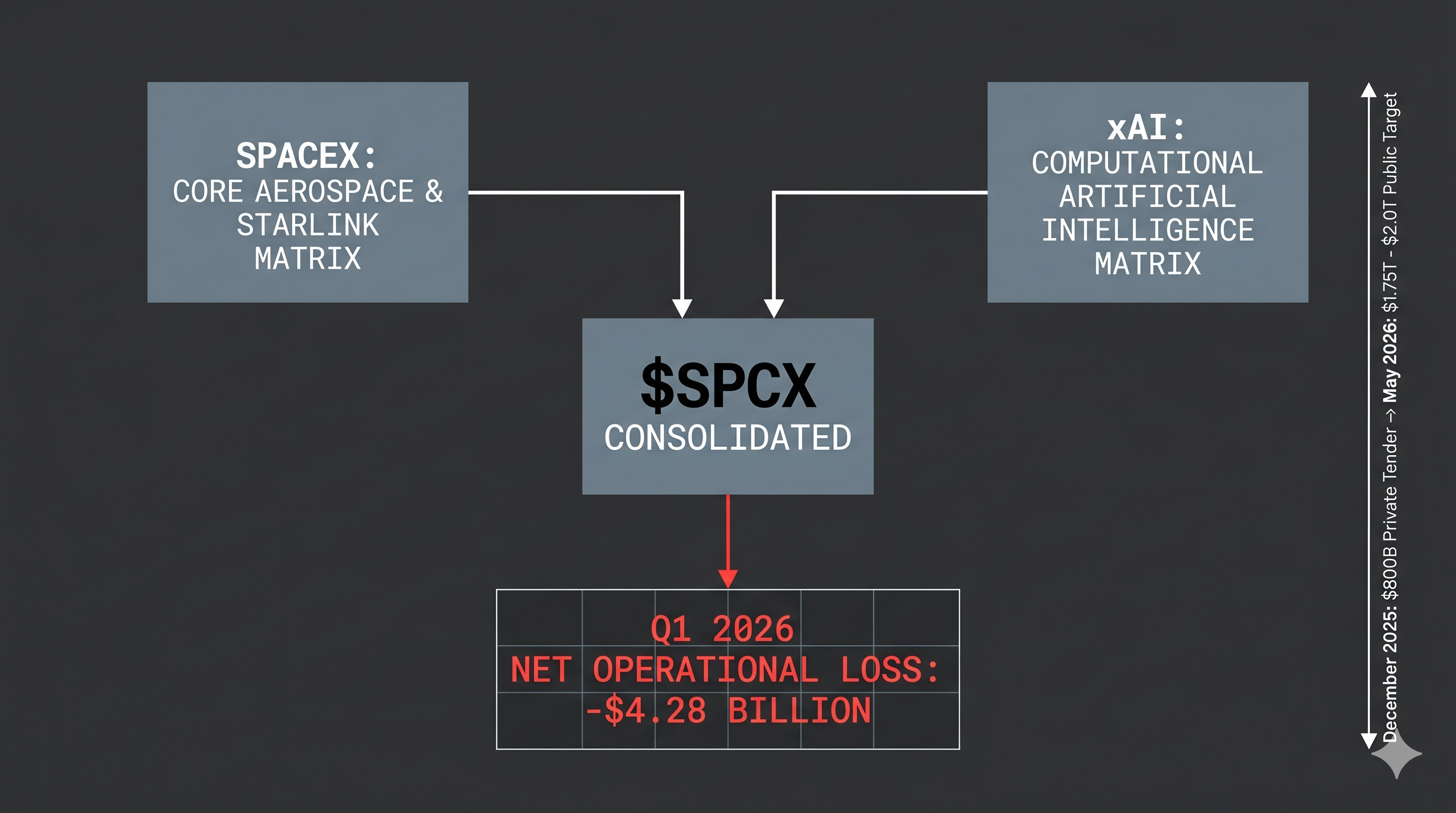

In February 2026, SpaceX completed an all-stock consolidation with xAI. This transaction abruptly merged a mature, cash-flowing aerospace firm with an early-stage, capital-intensive artificial intelligence matrix. While the aerospace and satellite components remain fundamentally viable on a standalone basis, the integration of xAI has introduced an unprecedented operational burn rate:

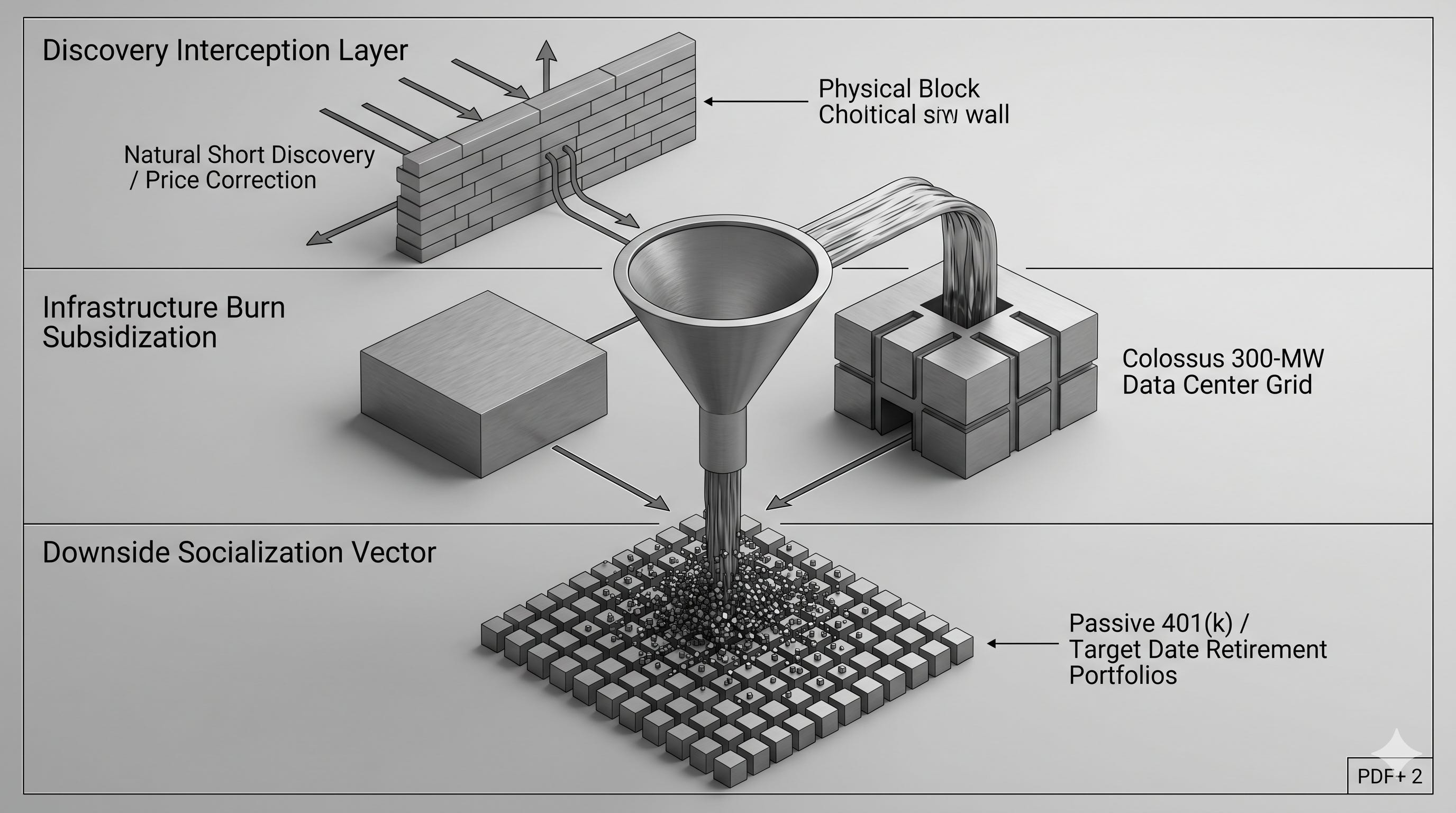

The Infrastructure Cost: Financing the continuous buildout and maintenance of the 300-megawatt “Colossus” data center grid.

Q1 2026 Financial Realities: The consolidated entity printed an unprecedented net loss of $4.28 billion for the first quarter of 2026 alone.

Valuation Discrepancies: Private secondary tender offers valued SpaceX at approximately $800 billion in December 2025. Following the all-stock xAI merger, the public target market cap was aggressively revised upward to between $1.75 trillion and $2.0 trillion—essentially pricing a pre-revenue, high-burn AI division at over $900 billion in implied equity value within a 180-day window.

CRITICAL DISCLOSURE DISCREPANCY (MAY 2026)

On May 20, 2026, the official S-1 prospectus cited a multi-year, contractually locked lease commitment from Anthropic, projecting revenue of $1.25 billion per month through May 2029 for Colossus capacity. However, subsequent public admissions on May 28 revealed the contract to be a highly volatile 180-day rolling lease with a 90-day mutual cancellation clause, instantly erasing over $37.5 billion in long-term revenue visibility.

2. MICROSTRUCTURE ALTERATIONS: THE INDEXING TRAP

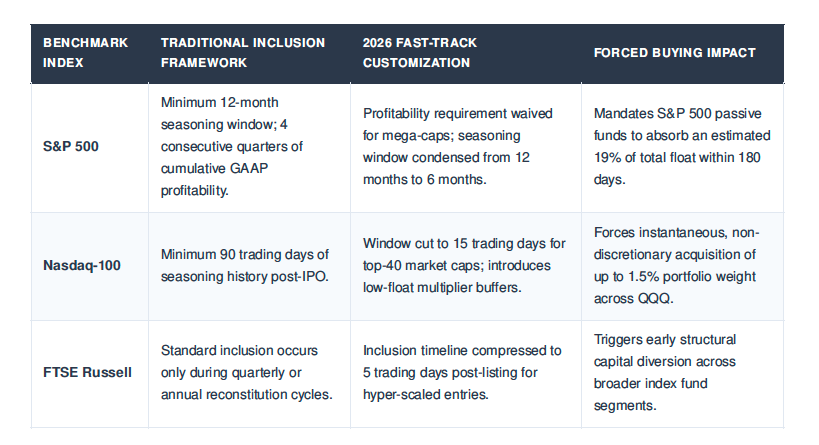

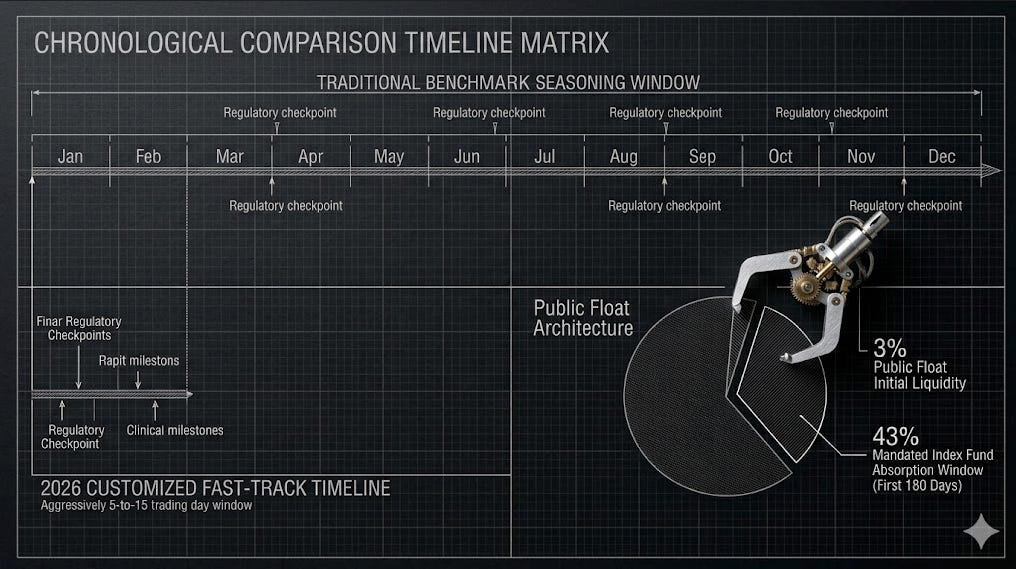

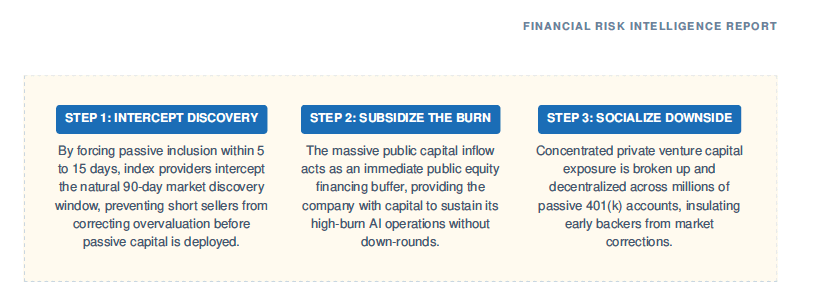

Under normal market guidelines established to preserve public investor safety, a multi-trillion-dollar entity with multi-billion-dollar quarterly GAAP losses and no public seasoning history would be barred from benchmark inclusion for months or years. To circumvent this, the three largest global index providers coordinated deep architectural modifications to their fast-track protocols.

The Float Adjustment Buffer Illusion

Proponents of these changes argue that passive capital is protected because indexes cap weightings based on *free-float* market capitalization (shares available to the public) rather than total market cap. With SpaceX floating a tightly constrained 3% to 5% slice of its equity, its initial index weighting in the S&P 500 will hover at a modest 0.08% to 0.12%.

However, the risk is not the absolute weighting; the risk is the concentration of buying volume relative to the actual float. Bloomberg Intelligence models confirm that index funds must absorb up to 43% of the *entire public float* within the first six months of trading. This extreme structural demand completely breaks traditional public market price discovery.

3. THE RISK TRANSFER PROTOCOL: POSTPONING THE RECKONING

The rapid, highly customized alteration of these indexing rules functions systematically as a private-to-public risk transfer mechanism. By engineering non-discretionary public buying demand almost immediately following the IPO, the market microstructure achieves three objectives for late-stage private insiders:

Structural Front-Running Costs

Because the exact dates of forced passive index buying are completely transparent and legally mandated, quantitative hedge funds and high-frequency market makers can trade ahead of the passive rebalance. These entities systematically accumulate $SPCX shares during the first 14 days, bidding the price to an artificial premium, and legally dumping their inventory directly into Vanguard, BlackRock, and State Street funds on Day15. The passive investor implicitly pays this structural transaction premium.

4. CAPITAL STACK EXPOSURE: WHO ABSORBS THE PREMIUM?

A forensic analysis of the $SPCX listing mechanics identifies three distinct demographics tasked with paying for the overvaluation premium.

I. The Passive Baseline (401k & Target Date Savers)

Passive retirement investors will experience losses not as a sharp, sudden portfolio collapse, but as long-term performance leakage. Because passive funds are forced to buy at the front-run, narrative-driven peak, the subsequent long-term correction of the stock to reflect actual cash-flow metrics prints permanent capital destruction directly into the index’s baseline performance.

II. Retail Allocatees (The 30% Float Red Flag)

The $SPCX S-1 prospectus reveals an anomalous structure: 30% of the entire IPO float is explicitly reserved for retail allocation via brokerage platforms such as Charles Schwab. In institutional market design, underwriters route nearly a third of a multi-billion-dollar float to retail accounts only when institutional desks show strong price sensitivity and resistance to the targeted valuation. These retail buyers act as direct, immediate exit liquidity for pre-IPO tender participants.

III. Legacy Tesla ($TSLA) Equity Holders

Because institutional desks manage the broader “Muskonomics” ecosystem as a single interconnected capital pool, assets are highly fungible. Following the initial leak of the SpaceX prospectus in April 2026, Tesla shares dropped 10.5% in 10 days as macro funds rotated out of $TSLA to build liquidity for the $SPCX listing. Post-IPO, any significant downward valuation adjustment in $SPCX will force cross-asset pairs trading and margin liquidations, causing legacy Tesla shareholders to subsidize the SpaceX premium via correlation contagion.

5. INSTITUTIONAL GAPS AND REGULATORY SAFE HARBORS

The ability of multi-trillion-dollar asset management complexes to navigate these structural conflicts of interest without triggering enforcement actions is permitted by specific regulatory gaps and safe harbors within Federal securities laws.

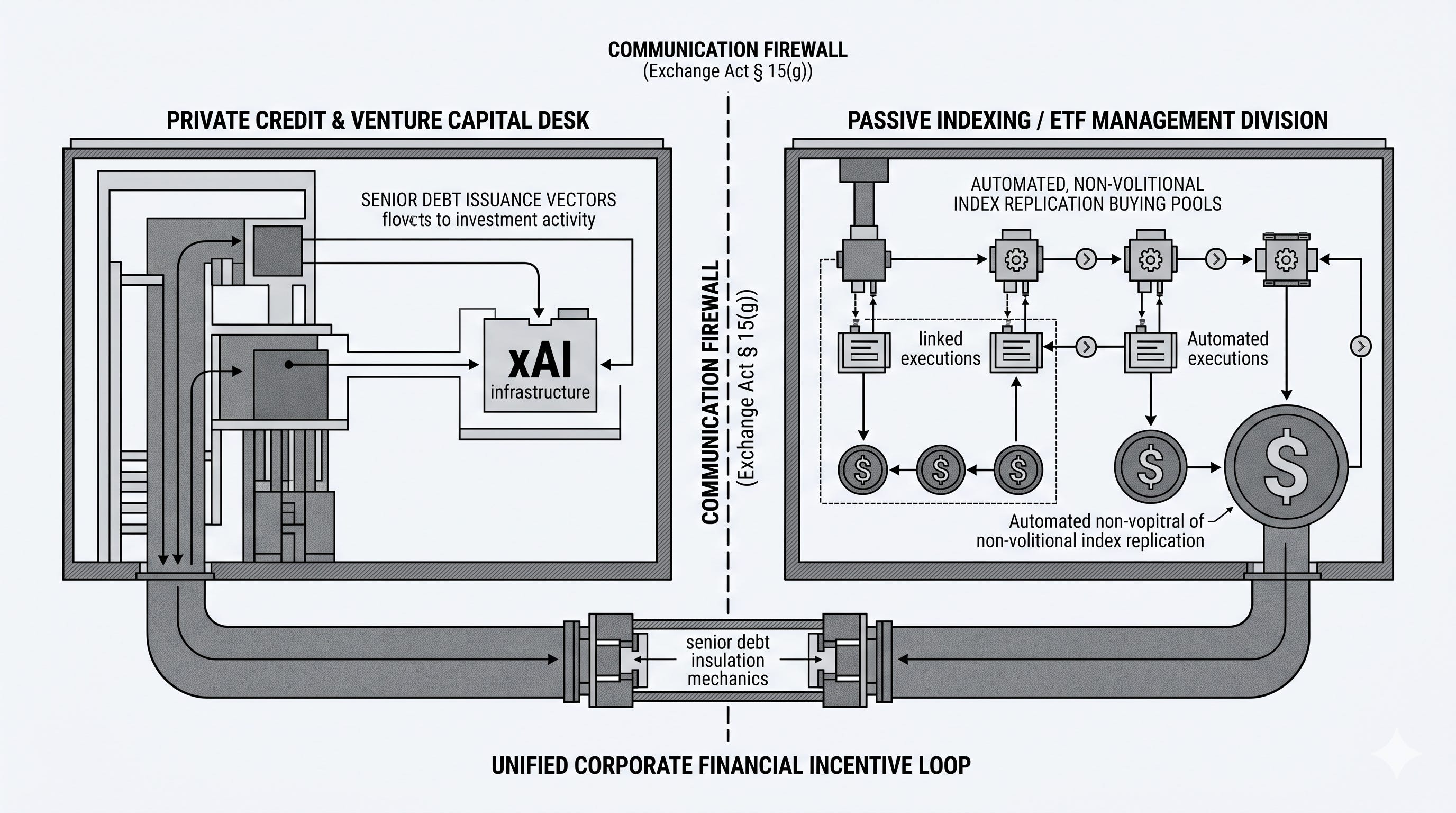

The “Non-Volitional” Defense (Investment Company Act of 1940 § 17(a))

Section 17(a) strictly prohibits self-dealing or the direct sale/purchase of securities between affiliated funds and desks. However, decades of SEC “No-Action” enforcement letters (e.g., *Evergreen*) have carved out a permanent exclusion for index-tracking vehicles. Because an ETF replicates a third-party benchmark automatically without human portfolio-manager discretion, the trades are legally deemed non-volitional. Thus, an asset manager’s private equity desk can exit an asset at an inflated valuation while its passive ETF desk simultaneously buys it, entirely immune from self-dealing liability.

The Publisher’s Exclusion (Investment Advisers Act of 1940 § 202(a)(11)(D))

Index providers effectively control capital allocation across global markets, yet they hold no fiduciary duties to the end-investor. Under Section 202(a)(11)(D), index providers operate under the **”Publisher’s Exclusion,”** legally classifying them as publishers of impersonal news and data rather than investment advisers.

Consequently, they can rapidly modify benchmark inclusion rules during closed corporate consultations with their largest fee-paying asset manager clients without disclosing conflicts or facing breach-of-fiduciary lawsuits.

Information vs. Incentive Firewalls (Exchange Act § 15(g))

While firms maintain strict information barriers required under Section 15(g) to halt the flow of material nonpublic information (MNPI), these barriers are strictly communicative—not structural. The absolute financial incentive of the parent corporation remains unified. A mega-manager’s private credit division can issue billions in high-yield bridge loans to finance xAI’s infrastructure, knowing with absolute certainty that the firm’s passive index division will automatically absorb public equity issues later, constructing a reliable public cushion underneath their senior private debt.

6. FORENSIC CONCLUSION & RED TEAM INSIGHTS

The consensus surrounding the $SPCX IPO represents a highly sophisticated, structurally insulated narrative loop. By combining a viable aerospace business with a capital-intensive, high-burn AI operation, private market sponsors engineered an unprecedented short-term valuation markup.

Realizing that the private venture capital and private credit ecosystems are unequipped to sustain a $4.28 billion quarterly operational burn rate indefinitely, institutional actors successfully leveraged the passive indexing pipeline to access public markets. By rewriting the entry rules of global benchmarks, they have eliminated natural price discovery and transformed passive public retirement funds into automated exit liquidity.

The forensic verdict is clear: the overpricing of $SPCX is a calculated risk-transfer event. While private market insiders concentrate real capital gains and insulate senior debt structures, the long-term premium decay will be quietly, systematically born by the passive index captive.

Legal Disclaimers & Disclosure Framework

1. Investigative Journalism & Editorial Notice

This document is published strictly for informational, educational, and independent investigative journalism purposes as part of the Protocol Zero ecosystem and The Vault publication. The contents herein represent the forensic analysis, system-engineering diagnostics, and editorial opinions of the author as of May 30, 2026. This research does not constitute a coordinated media campaign, nor is it intended to maliciously target any specific corporate entity, executive, or underwriting syndicate.

2. Not Financial, Legal, or Investment Advice

Nothing contained in this white paper constitutes a solicitation, recommendation, endorsement, or offer to buy or sell securities, options, futures, or other financial instruments.

Independent Analysis: The structural analysis of the $SPCX IPO, benchmark index parameters, and corporate matrix correlation represents an adversarial risk-mapping exercise, not an investment thesis.

No Fiduciary Duty: The author is an independent investigative reporter and forensic auditor, not a registered investment adviser, broker-dealer, or financial planner. Readers must not rely on this document to make investment decisions, and are urged to conduct their own due diligence and consult with licensed financial professionals before allocating capital.

3. Forward-Looking Statements & Predictive Analysis

This report contains numerous forward-looking statements, estimations, and predictive market-structure models regarding the upcoming June 12, 2026 listing of SpaceX, anticipated passive index fund flows, and prospective corporate capex timelines.

Inherent Uncertainty: Forward-looking statements are inherently subject to significant risks, market shifts, regulatory interventions, and macroeconomic changes.

No Guarantee of Outcome: Actual market outcomes, index inclusion weightings, regulatory actions, and corporate financial performance may differ materially from the projections and red-team simulations outlined in this text. The author assumes no obligation to update or revise any forward-looking statements should underlying conditions shift.

4. Data Sourcing, Leaks, and Proprietary Metadata

The financial metrics, operational data, and contractual terms evaluated in this white paper—specifically regarding the xAI merger, the Colossus data center specifications, and the Anthropic lease visibility—are derived from a combination of publicly available SEC filings (S-1 prospectus frameworks), verified corporate statements, and widely reported internal institutional leaks.

Good Faith Accuracy: While every effort has been made to verify the mechanical and mathematical accuracy of the information at the time of publication, the data is subject to change or correction by the issuing companies and underwriting syndicates.

Disclaimer of Liability: The author explicitly disclaims any and all liability for inadvertent inaccuracies, omissions, or subsequent revisions made to official registration statements by third-party corporate actors post-publication.

5. Independence & Conflict Disclosure

The author maintains complete editorial and financial independence. The author holds no direct long or short equity positions, derivatives, options, or debt instruments in SpaceX ($SPCX), Tesla ($TSLA), xAI, or any of the specific exchange-traded funds (ETFs) or asset management firms (Vanguard, BlackRock, State Street, Fidelity) cited in this report. No compensation, underwriting allocations, or access privileges were provided by any corporate entity or financial institution to influence the findings, verdict, or presentation of this research.